In order to contribute to the national and European economic debate, the Banque de France periodically publishes macroeconomic forecasts for France, constructed as part of the Eurosystem projection exercise and covering the current and two forthcoming years. Some of the publications also include an in-depth analysis of the results, along with focus articles on topics of interest.

Introduction

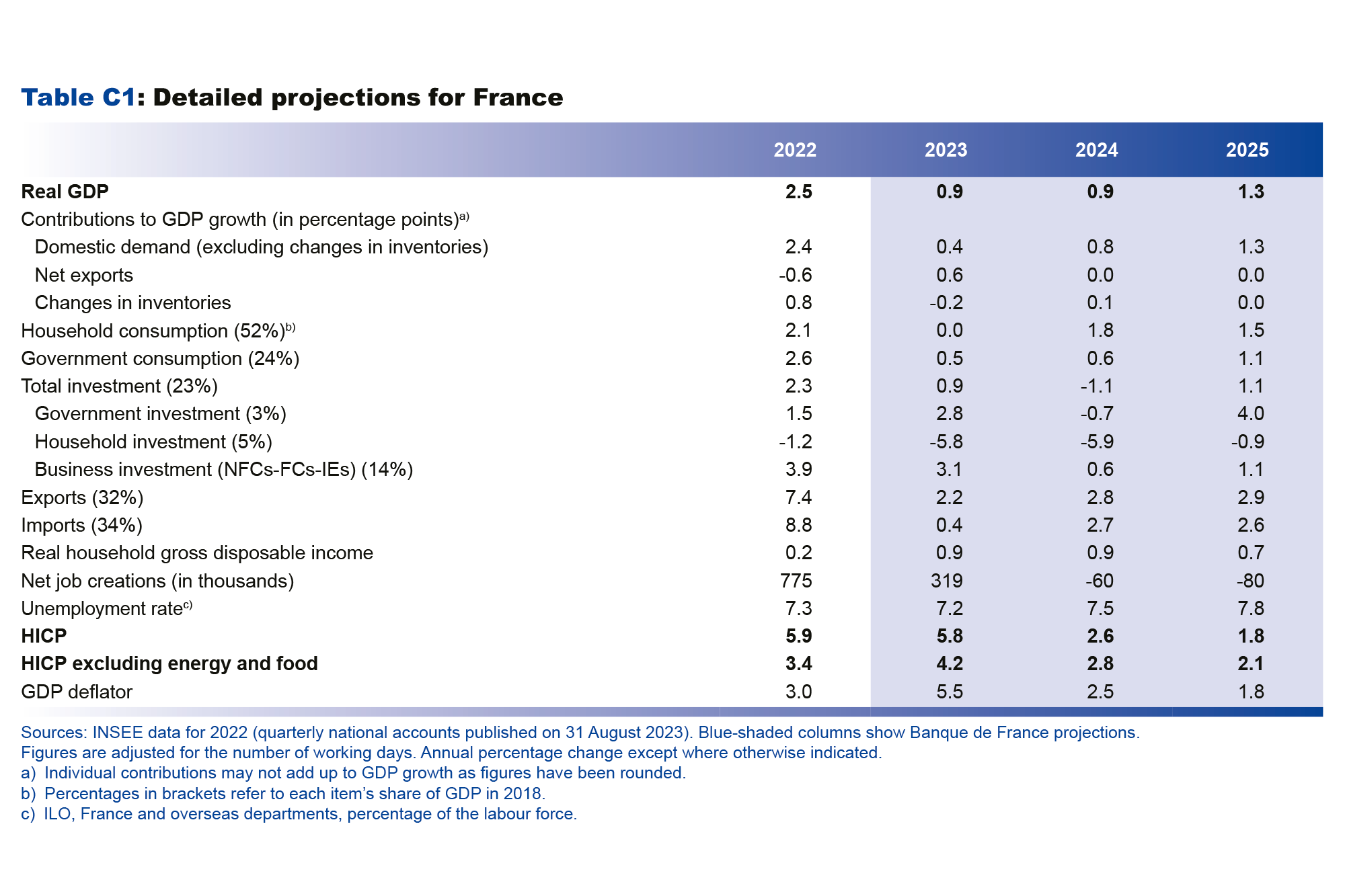

• Compared with our June projection, we expect very similar cumulative growth between now and 2025, but with a different timeline: higher in 2023, followed by a more gradual recovery. The French economy should therefore gradually overcome inflation without slipping into recession, even though an unfavourable international environment may weaken the recovery. On the back of sustained growth in the first half of the year, our GDP growth forecast for 2023 has been revised up to 0.9%. Going forward, the upward revision of energy prices over our projection horizon, and especially a downward revision of foreign demand for French goods and services, have led us to lower our forecasts slightly for 2024 and 2025 to 0.9% and 1.3%, respectively.

• After peaking in early 2023, headline inflation should continue to subside, falling to 4.5% in the fourth quarter of the year. The new increases in energy prices in the summer of 2023 are different to those witnessed in 2022 and, based on current market expectations, they should only be temporary. Aside from possible jolts to the most volatile components, inflation is expected to fall markedly right across our projection horizon. The trend first witnessed in industrial goods and then in food prices, should become more widespread and finally reach services. Provided there are no new shocks to commodity import prices, headline inflation should come back to around 2% in 2025.

• We forecast a moderate fall in employment, reflecting the delay in adjusting to the economic slowdown observed since late 2022. Consequently, the unemployment rate is forecast to gradually increase over our projection horizon to reach 7.8% in 2025, which is actually below the pre-pandemic rate.

• Although perceptions continue to be rather negative, household purchasing power should grow over the projection horizon, due mainly to a recovery in real wages. Businesses are expected to remain resilient and the corporate margin rate should remain slightly higher than the pre-Covid rate. However, the downside of this favourable situation for households and businesses over the projection horizon is that the government debt ratio should remain at around 110% of GDP in 2025. This is markedly higher than the euro area average (88.5%), which is expected to decline by around 3 points of GDP between 2022 and 2025.

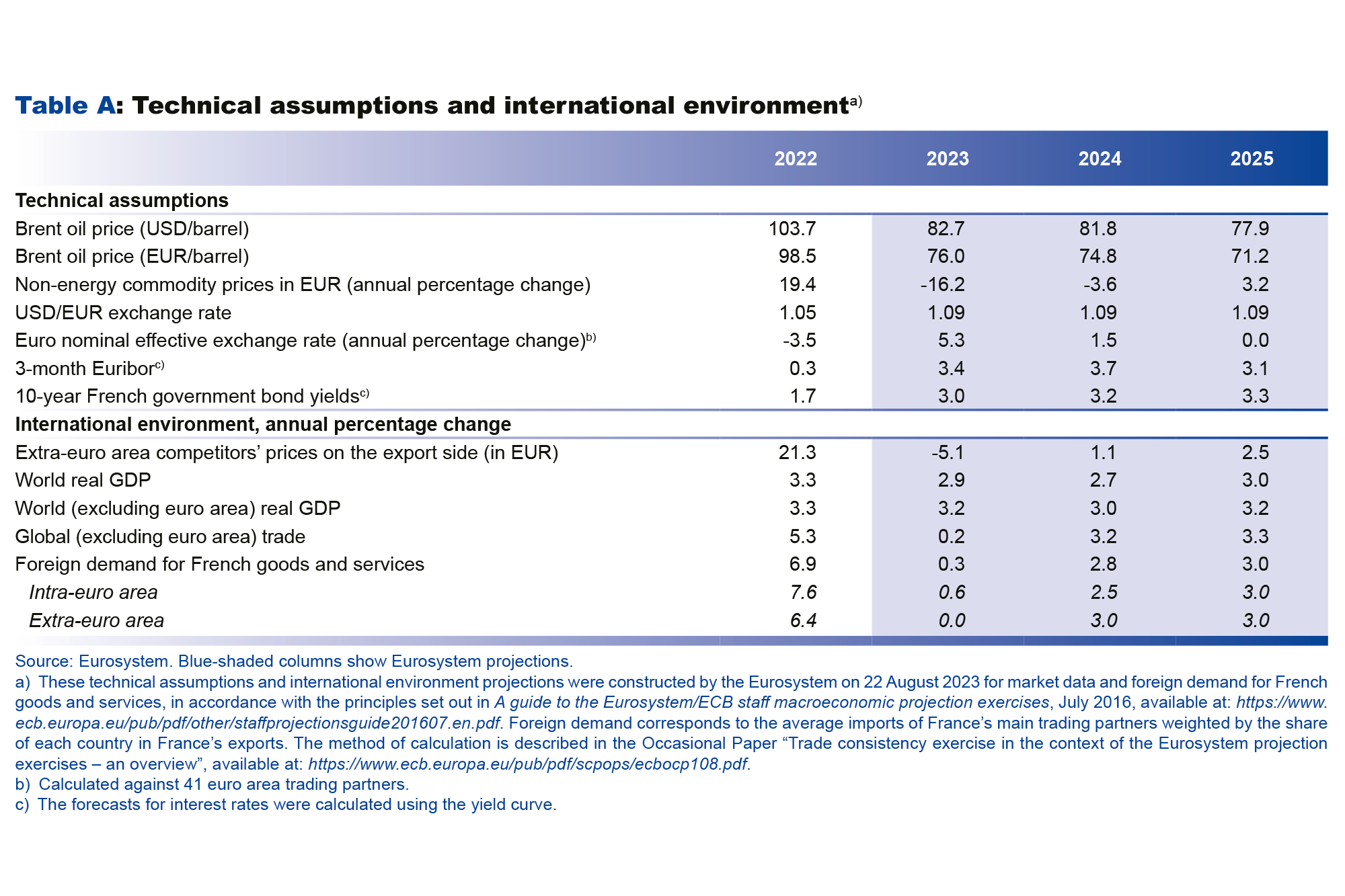

These projections were finalised at the beginning of September and incorporate final HICP (Harmonised Index of Consumer Prices) inflation figures for July, published on 11 August 2023. They incorporate the detailed figures for the second quarter 2023 national accounts published by INSEE on 31 August 2023, and the economic data from the Banque de France’s monthly business survey for August. They also draw upon Eurosystem technical assumptions, for which the cut-off date is 22 August 2023.

Aside from some jolts to energy prices, the underlying trend should be for a clear fall in inflation, with the reading coming down gradually toward 2% by 2025

HICP inflation has been falling quite sharply for several months. After peaking at 7.3% in February 2023, it fell to 5.1% year-on-year in July 2023. Although it went back up to 5.7% year-on-year in August 2023, reflecting the spike in energy prices (rise in oil prices and the 10% increase in regulated electricity prices effective from 1 August 2023), this upward movement should only be temporary (see below). Inflation excluding energy and food has also been falling for several months. It was 4.0% year-on-year in August 2023, down from 4.4% in May-June, and from the peak of 4.7% in April.

Over 2023 as a whole, year-on-year headline inflation is predicted to gradually decline from 7.0% in the first quarter to 4.5% in the fourth quarter (see Chart 1). This also goes for year-on-year inflation excluding energy and food, which is forecast to fall from 4.4% to 3.7% over the same period. In annual average terms, headline inflation for 2023 is forecast at 5.8%, while inflation excluding energy and food should be 4.2%. This latter figure has been revised downwards compared with our June projection, which was for 4.4% inflation in annual average terms.

On a more detailed level, the fresh increases in energy prices in the summer of 2023 are nothing like those witnessed in 2022, which were driven by the consequences of the Russian invasion of Ukraine (see box). As regards food inflation, we expect retail prices to gradually stabilise as most of the price increases negotiated at the start of the year between producers and large retailers have already been passed on. The resumption of trade negotiations over the summer ultimately had no significant impact, and our projections do not currently factor in any specific downward effect of future price negotiations. Year-on-year, food inflation should continue to fall in the second half of 2023.

Manufactured goods inflation should also moderate rapidly beginning in the second half of 2023, reflecting the marked drop in industrial producer prices that began in the first quarter on the back of falling import prices. In contrast, services inflation is expected to remain stickier owing to persistent wage pressures, especially with the upward revision of the SMIC (minimum wage) and rises in industry-level negotiated wages. Moreover, we have factored in the extension of the 3.5% cap placed on the rent reference index in metropolitan France through to the first quarter of 2024, which should help to contain the increase in rents. The peak in services inflation is ultimately expected to be delayed until the fourth quarter of 2023, when the year-on-year rate should reach 4.5%, and then only start to come down in early 2024.

In 2024, under the assumption of the easing of commodity prices currently factored in by futures markets, all components of inflation should fall. The main driver of inflation should then be services prices (see Chart 2), which are expected to continue being supported by delayed hikes in wages and rents and the ongoing margin recovery expected in some sub-sectors. In annual average terms, headline inflation is seen falling to 2.6%, while inflation excluding energy and food should recede more slowly to 2.8%. By the fourth quarter of 2024, year-on-year headline inflation should have come down to 2.2%.

In 2025, headline inflation and inflation excluding energy and food should continue to decline, reaching 1.8% and 2.1%, respectively, in annual average terms. This reflects the dual impact of the ongoing normalisation of commodity prices (energy and food) and the gradual transmission of monetary policy tightening to core inflation. Services prices in particular should start to slow, and should only increase at an annual average rate of 3% in 2025, reflecting smaller nominal wage increases than in the two previous years (that will nonetheless allow real wages to rise; see later section).

Box : The scale of the recent jump in oil prices is different to the multiple commodity price shocks of 2021-22 and does not therefore invalidate our prediction of a downward trajectory for inflation

In summer 2023, the price of oil rose, mainly due to a decision on the part of OPEC and Russia to restrict supply, leading to fears that the fall in headline inflation that began in the first half of 2023 would be interrupted. However, these new price rises are of a different nature and nothing like the price shocks experienced in 2021 and 2022, which caused severe stress across all commodity markets (post-Covid recovery and supply difficulties followed by the Russian invasion of Ukraine, triggering a massive energy crisis), affecting the price of oil, gas and electricity, foodstuffs and certain metals.

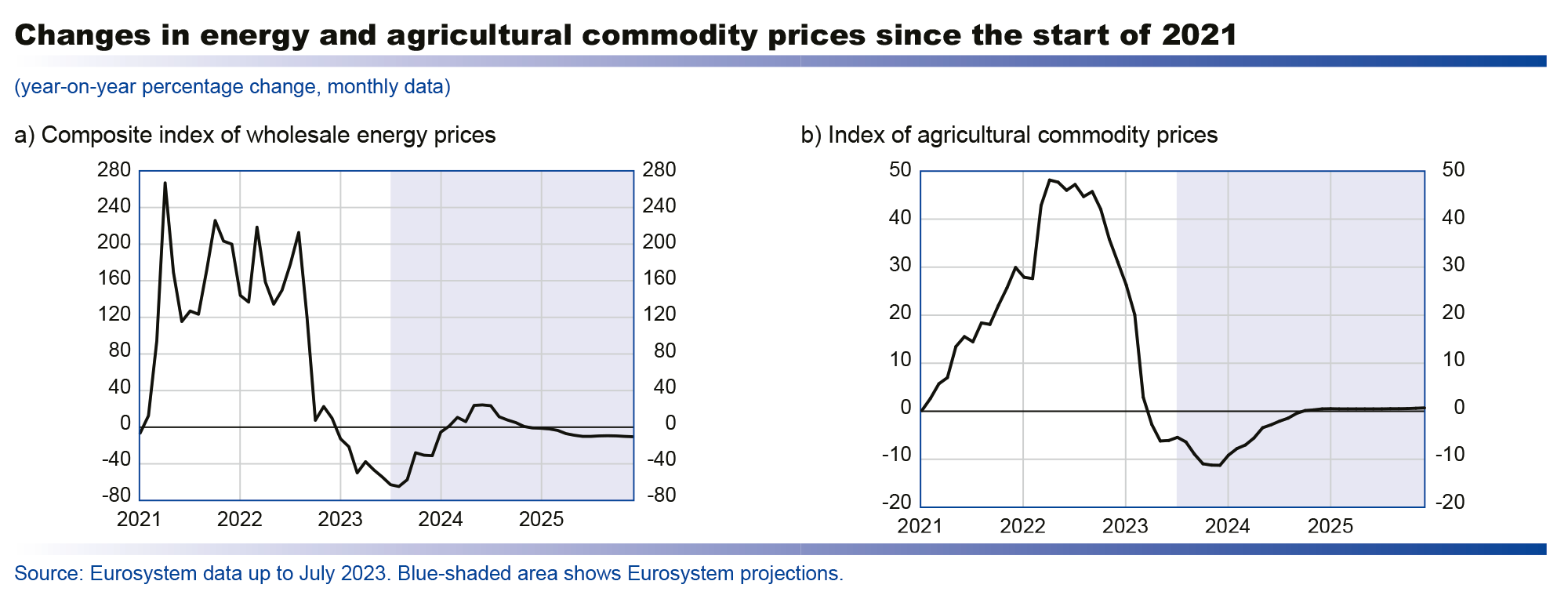

In the wake of the Ukrainian crisis, fears over European gas supplies pushed wholesale gas prices to unprecedented levels. This pressure also spread to wholesale electricity prices, which are largely determined by the price of gas because of the way the European energy market currently works (in France’s case, this contagion was exacerbated by problems encountered at its nuclear reactors). Overall, the year-on-year increase in the wholesale energy price – measured here by a composite index of wholesale gas and oil prices, expressed in euro per barrel of oil equivalent – hit highs of over 200% during 2021 and 2022 (see chart), before subsequently coming back down, but remaining at a higher level than in first-half 2021. At the same time, the year-on-year increase in agricultural commodity prices peaked at 48% in April 2022, mainly due to the slump in Ukrainian and Russian cereal exports.

The situation is very different in the summer of 2023. As regards fossil fuels, the price shocks currently only affect oil and not gas, as fears of supply difficulties have eased considerably thanks to Europe's reduced dependence on Russian gas. Based on year-on-year price expectations on futures markets, the composite energy price index should gradually start climbing in summer 2023 to peak at 24% in June 2024. At the same time, agricultural prices are even expected to fall slightly as international markets gradually settle down again, although the price outlook on futures markets remains subject to considerable uncertainty. Moreover, in August 2023, the French government decided to increase the regulated electricity price by 10% to phase out the energy price shield. However, this corresponds to a normalisation of final prices rather than a new shock to wholesale prices.

In our projection, the energy component of French HICP inflation (Harmonised index of consumer prices) should decline between 2022 and 2025, from a jump of 24% in 2022 before virtually stabilising in 2025. The increase in the food component of French HICP inflation is expected to peak in 2023 at nearly 12%, before falling back to a little under 2% in 2025. Naturally, these projections are subject to the information currently available (see also the section on the risks to activity and inflation).

Growth is set to be more resilient than expected in 2023, followed by a slightly more gradual recovery, leaving forecast cumulative growth in GDP between now and 2025 very close to our June projection

Whereas economic activity stagnated in the first quarter of 2023, GDP growth figures for the second quarter surprised on the upside. While we were expecting quarterly growth of 0.1%, it actually came in at 0.5%, boosted in particular by coking and refining activity (following the end of strikes in refineries), and by a return to normal electricity production. Because these are catch-up phenomena rather than one-off events, we do not expect a mechanical downward adjustment of growth in the third quarter. The main one-off factor that could lead to an adjustment – the delivery of the MSC Euribia cruise liner – essentially concerns exports and changes in inventories, and, according to INSEE, should only have a limited impact on activity. Conversely, strong second quarter growth does not signal the start of a strong recovery. More specifically, while the carry-over effect for 2023 growth was 0.8% at the end of the second quarter, it was only 0.2% for the contribution of domestic demand excluding inventories. Growth is expected to remain moderate over the third quarter of 2023, at between 0.1% and 0.2%, according to the most recent Monthly Business Survey published in early September, and it should remain at around 0.2% in the fourth quarter. Overall, the surprise of the second quarter has caused us to revise our annual growth forecast for 2023 upwards compared with the June projection. For 2023 as a whole, GDP growth is predicted to be 0.9% (see Chart 3), up 0.2 percentage points on the June projection.

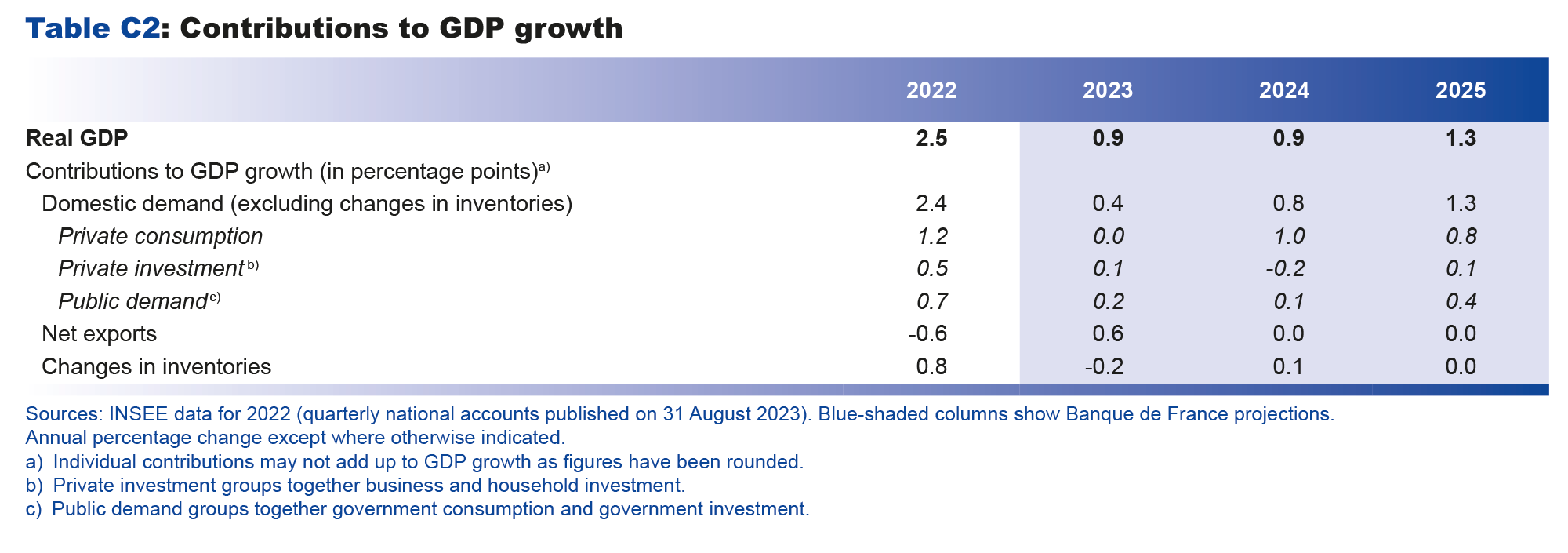

Over the rest of our projection horizon, the recovery in activity should be underpinned by a rebalancing of growth in favour of domestic demand, whose contribution (excluding inventories) should increase by 0.8 percentage point in 2024 and 1.3 percentage points in 2025, after increasing by 0.4 percentage point in 2023. The 0.9% GDP growth we forecast for 2024 would therefore mainly be driven by domestic demand excluding inventories (contribution of 0.8 percentage point, see Table C2 in the appendix), while the contribution from external trade should be zero in 2024 (after 0.6 percentage point in 2023). In 2025, GDP growth should rise to 1.3%, still buoyed by the twin domestic growth drivers of household consumption and business investment. Household consumption should benefit from the positive impact on purchasing power of a return to inflation of around 2%, partly attenuated by the decrease in employment, a delayed consequence of the past economic slowdown. The recovery in demand should also enable business investment to begin to accelerate again. Overall, because growth has been revised upwards for 2023, and downwards for 2024 and 2025, forecast cumulative GDP growth between 2022 and 2025 should be close to the June projection.

Over our projection horizon, the terms-of-trade shock resulting from Russia’s invasion of Ukraine (defined as the change in import expenditure net of export income since 2021 that is attributable to price changes, measured as a percentage of GDP), should gradually subside as commodity prices fall (see Chart 4) and past shocks are passed through to French export prices. From approximately 1.5% in 2022, we expect it to fall to around 0.5% of GDP in 2023 (again compared with 2021). It should then stabilise at this level over the rest of the projection horizon. The dissipation of this external tax shock should improve the situation of the different French economic agents: households in terms of purchasing power, businesses in terms of profit margins, and general government in terms of the government budget balance, although this is in a worse state now than before the Covid crisis.

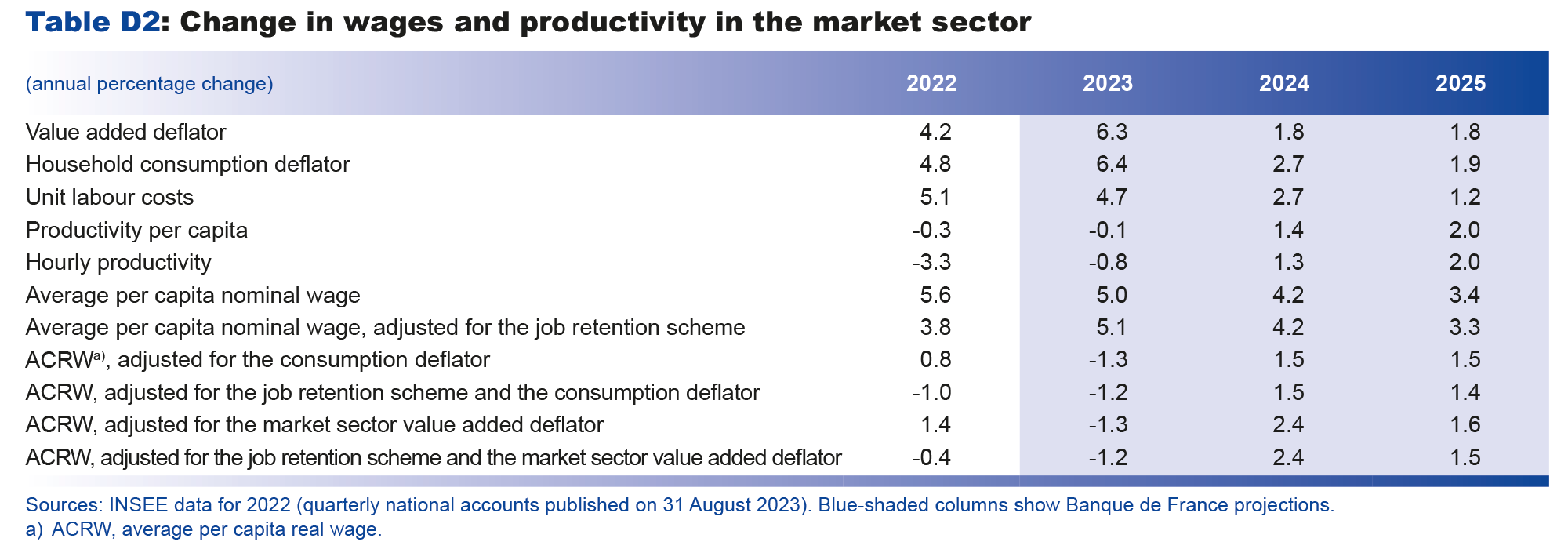

Given the fall in inflation, real wages should rise substantially in 2024-2025 in spite of the slowdown in nominal wage growth

The growth in average per capita wages, as shown by the year-on-year increase of 5.0% in the second quarter of 2023, notably reflects the payment of large one-off bonuses called primes de partage de la valeur (PPV – value-sharing bonus), which replaced the prime exceptionnelle de pouvoir d’achat (PEPA – exceptional purchasing power bonus). The monthly base wage, which excludes bonuses, was up 4.6% year-on-year in the same quarter.

In our projection for 2023, we expect PPV payments to remain high and, alongside seniority-based and individual pay rises as well as staff turnover, they should help to maintain the gap seen recently between year-on-year growth in the average per capita wage and the monthly base wage. Growth in the average per capita wage is expected to peak in 2023, with an average annual increase of 5.1% (adjusted slightly downward from our projection of 5.4% in June, in both cases adjusted for short-time work schemes). However, the real average per capita wage is predicted to fall in 2023, as it did in 2022. In 2024 and 2025 however, the real average per capita wage should return to a clearly positive growth rate. Nominal per capita wage growth is set to slow, but by less than prices (see Chart 5). This mismatch between inflation and nominal wage growth is the result of the annual nature of wage renegotiations as well as delayed indexation of the minimum wage.

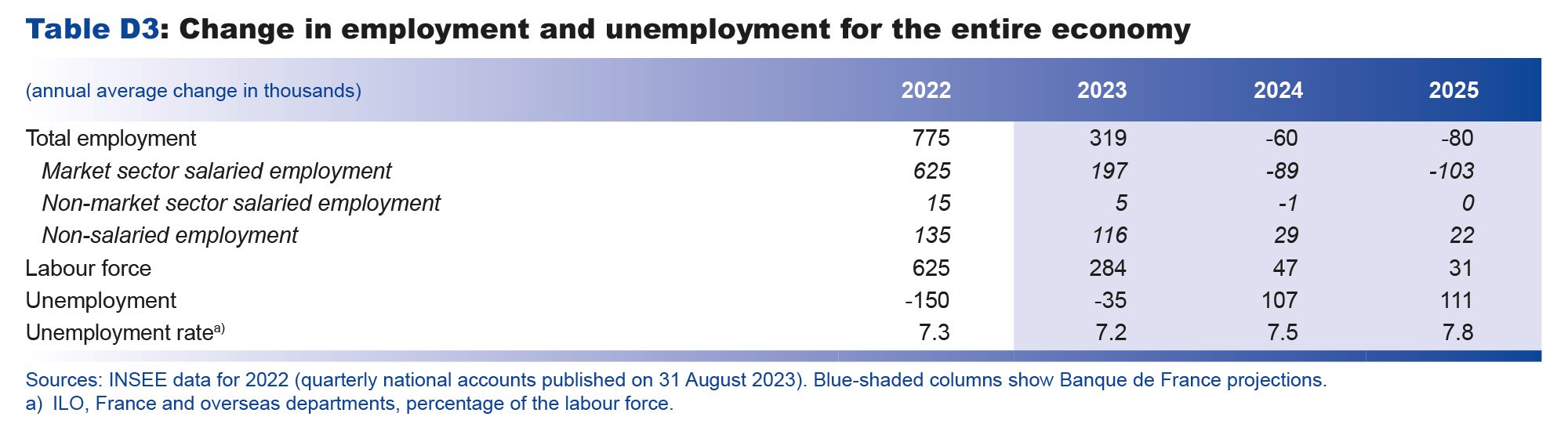

Employment is predicted to fall a little after the especially positive trends of recent years

Net salaried job creations have remained strong over the recent period, however they are starting to taper off: they slowed to over 41,000 jobs in the second quarter across the economy, compared with over 100,000 jobs per quarter at the start of 2022. Based on the latest short-term indicators for the third quarter of 2023, we expect net salaried job creations, but at an even more sluggish pace.

The upward revision of employment in the annual accounts for 2022 has helped widen the gap between labour productivity and its trend in the second quarter of 2023 compared with our June forecasts. Going forward, firms should gradually adjust their workforces as growth becomes progressively stronger, gradually reducing this productivity gap, although the gap will not have closed completely by the end of our projection horizon (see Chart 6).

The unemployment rate edged up slightly in the second quarter of 2023 (by 0.1 percentage point), despite the positive surprises concerning GDP and employment, reflecting a stronger-than-expected increase in the labour force. Over the projection horizon, the rise in the unemployment rate should also be attributable to the labour market’s delayed reaction to the past slowdown in activity. The rise in unemployment is therefore predicted to be slightly higher than in our June projection, due both to the higher than expected reading in the second quarter and to slightly slower growth in 2024 and 2025, albeit with a time lag. Consequently, the unemployment rate, which stood at 7.2% in the second quarter of 2023, is forecast to gradually increase to 7.8% by the end of 2025 (see Chart 7). This rate should still be lower than it was in 2019.

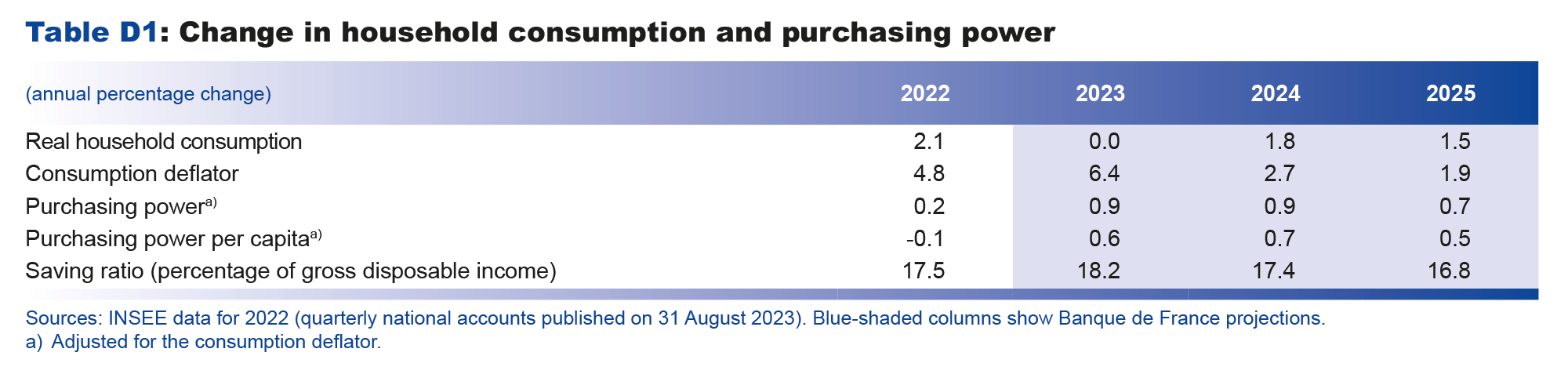

After stagnating in 2023, household consumption should start to rise again from 2024 onwards

Purchasing power per capita, or real gross disposable income per capita, is now expected to rise by 0.6% in 2023 (see Chart 8), whereas in June we forecast a fall of 0.4%. This sizeable upward revision stems primarily from the incorporation of the quarterly national accounts published since then by INSEE, which in mid-2023 show a 1% carry-over effect for growth in the purchasing power of real disposable income. This reflects higher-than-expected growth in non-wage income (especially rental and net interest income). In contrast, our forecast for real wage income remains unchanged for 2023: it should continue to be driven by further strong employment growth in the first half, which should more than offset the fall in the real average wage per capita.

Starting in 2024, there should be an inversion in these two drivers of wage income: employment is no longer expected to provide support, but nominal wages should outstrip inflation. Fiscal support measures should also provide a boost to household purchasing power, notably the abolition of housing tax for the final segment of the population, the increases in pensions and public sector pay, and the decision to remove the electricity price shield only gradually, up to the end of 2024. As a result, purchasing power per capita is projected to continue rising at a rate of around 0.5% a year in 2024 and 2025.

If we look at the longer-term picture, starting in 2019 before the two major shocks to the French economy (the public health crisis and the Ukraine crisis), purchasing power per capita should be about 4% higher in 2025 than before the Covid crisis. This is attributable first to salaried employment, which is expected to be 6% higher in 2025 than before Covid. However, after the inflationary surge in 2022 and 2023, the purchasing power of average per capita wages should be close to its pre-Covid level in 2025.

For a number of reasons, perceptions of the rise in purchasing power per capita are more negative than this projection. First, it is an average forecast, and individual situations may vary depending on income levels and geographical location. Second, as explained above, total income includes all income items (including social security transfers net of tax) and not just wage income, but the latter probably has the biggest impact on household perceptions of their purchasing power. Lastly, and most importantly, day-to-day perceptions of inflation may take greater account of frequent purchases such as petrol and food products, than of headline inflation measured by INSEE, which is used to calculate total purchasing power.

The household saving ratio was exceptionally high in the second quarter of 2023, which cannot be fully explained by the standard determinants of consumption (purchasing power and interest rates). This may in part reflect continuing strong uncertainty, which is leading to precautionary saving behaviour. Another explanation could be households’ sensitivity to the real balance effect, which may be encouraging them to maintain high savings inflows to compensate for the erosion of existing savings by inflation. Our forecast is for households to reduce their saving ratio as these two factors subside, helping to shore up consumption over the medium term. Consequently, the saving ratio is seen declining gradually over our projection horizon, falling to 16.6% in the final quarter of 2025 (see Chart 9), although this is still well above its pre-Covid level (15.0%). However, the uncertainty surrounding the saving ratio in the wake of the major, unprecedented shocks of the last few years makes forecasts for this variable more uncertain than those for other macroeconomic variables (see later section on the risks to activity and inflation).

In light of these factors, after stagnating in 2023, household consumption is projected to rise again in 2024 and 2025, by 1.8% and 1.5% respectively, exceeding purchasing power gains. Household investment, in contrast, has fallen over the recent period as financial conditions have normalised, and is expected to remain on a downward trend for several quarters before picking up again during 2025.

The corporate margin rate should return to near its pre-Covid level in 2025, while business investment should prove fairly resilient over the period

The non-financial corporation (NFC) margin rate increased in the second quarter of 2023, although this masks contrasting sectoral trends that are most probably temporary. The margin rate rose particularly sharply in energy-related sectors, which only partially passed on falls in input prices to producer prices. This effect should prove transitory and we expect producer prices to grow more slowly over coming quarters. However, over the medium term, profits should be boosted by two factors. First, the recovery in productivity growth, reflecting the delayed adjustment of the labour market to the economic slowdown, should offset the impact of stronger real wage growth on the NFC margin rate. Second, profits should be buoyed slightly by the abolition of the cotisation sur la valeur ajoutée des entreprises (CVAE – corporate value added contribution), which was originally supposed to take the form of a second cut concentrated in 2024, but will now be spread over four years. By the end of the projection horizon, in 2025, the NFC margin rate is predicted to be 32.1%, which is slightly above its pre-Covid level (see Chart 10).

Business investment has proved resilient for a number of years: despite the Covid crisis and invasion of Ukraine, it has grown by more than activity each year since 2020. This is mainly attributable to high levels of investment in information and communication technology. Consequently, monetary policy tightening and the restriction of the credit supply are only expected to cause a temporary slowdown in investment, and not a contraction (see Chart 11). In the medium term, investments in the climate and energy transition could replace those linked to the digital transformation as a driver. Business investment is therefore predicted to remain resilient over the projection horizon, although it should grow a little more slowly than activity. However, there are risks to this forecast for the investment trajectory (see later section on the risks to activity and inflation).

The French government debt ratio is merely expected to stabilise, remaining persistently higher than the euro area average

This forecast incorporates the most recent measures officially announced before its finalisation date in August 2023. It does not take account of the new measures and information to be set out in the draft budget for 2024, which will be incorporated into our December projection. On this basis, in line with our June publication, we expect the government debt ratio to merely stabilise, remaining at around 110% of GDP (see Chart 12). France’s debt ratio should thus remain persistently higher than the euro area average, which is seen shrinking by 3 percentage points between 2022 and 2025, to 88.5% of GDP in 2025. The gap between France’s debt ratio and the euro area average is projected to widen from 15 percentage points before the Covid crisis to 20 percentage points by the end of the projection horizon.

The baseline scenario for the international environment does not incorporate new large shocks, but should be less favourable for exports up to 2025

After rebounding in the wake of the Covid crisis, global trade has been slowing since the start of 2022. This relative sluggishness should be followed by a very gradual and uncertain recovery. The outlook for China in particular looks weak as the latest economic indicators surprised on the downside. But the situation in the euro area should prove even more detrimental for French exports. Since our last projections in June, the biggest downward revisions to demand for French goods and services have been to intra-euro area demand. Import projections have notably been revised downwards for Spain and Italy in 2023, and even more so for Germany in 2024.

Against this backdrop, French exports nonetheless surprised on the upside in the second quarter, with transport equipment sales holding up particularly well – due in part to the one-off delivery of the cruise liner MSC Euribia – and the tourism sector posting a rebound. Over 2023 as a whole, French exports are seen rising faster than foreign demand for French goods and services, meaning that the country should continue to gradually win back market share lost during the public health crisis. In 2024 and 2025, we expect France’s market share to remain stable, as positive and negative drivers counterbalance each other. On one hand, the past appreciation of the euro effective exchange rate should make French exports slightly less competitive outside the euro area. On the other hand, French exports should be boosted by a potential rebound in the aeronautics and tourism sector.

The risks to our baseline projections for activity and inflation are on the whole balanced

The risks to energy markets have changed since the winter of 2022-23. The risk of interruption of gas and electricity supplies (linked to the halting of Russian gas deliveries and difficulties with France’s nuclear reactors) has been replaced by risks to gas and oil prices linked to mismatches in supply and demand. In the gas market, the risks notably stem from supply pressures in liquefied natural gas, as shown by recent concerns over the threat of strikes in Australia. In the oil market, there are uncertainties over both sides of the supply/demand balance: the geopolitical situation is continuing to weigh on supply (as shown by OPEC and Russia’s recent decisions to cut supply), but the downward risk to activity in China could lower demand.

In the case of global demand, the main downside risks are also from China, where recent figures have confirmed the slowdown in activity over the past few months, and concerns are growing over the property market crisis and the state of the jobs market (youth unemployment). The risks have become more balanced in the United States, where the threat of a recession or “hard-landing” has receded significantly.

Regarding French domestic demand, the risks to household consumption are more to the upside, while those to business investment are to the downside. We cannot rule out a sharper-than-expected rebound in consumption, as our baseline scenario factors in a historically high saving ratio up to the end of the projection horizon. While this high ratio is a negative signal for consumption in the near term, it does give households more room to increase their spending over the medium term, once current uncertainty has subsided, especially over energy markets. Conversely, while our baseline scenario is for business investment to slow but not fall, the tightening of financial conditions could weigh more heavily than expected.

There are also a number of specific risks to our forecast for French inflation. Our baseline scenario is for profits in the refining and distribution of petroleum products to return quickly to their long-term equilibrium level. But if they remained higher for longer, prices would come under upward pressure. On the downside, however, monetary policy could have a stronger or faster impact on inflation than we currently predict.

Download the PDF version of this document

Updated on 25 March 2024